Article content

Canada ranks among the countries hardest hit by higher interest rates in the developed world, but a new report says it didn’t have to be that way.

Longer mortgages terms would have lessened the pain, says new report

Canada ranks among the countries hardest hit by higher interest rates in the developed world, but a new report says it didn’t have to be that way.

Article content

Since the Bank of Canada began hiking rates in 2022, the debt-servicing ratio of Canadian households has soared to one of the highest among the advanced economies. But if longer mortgage terms had been more prevalent and attractive, the payment shock would have been much more manageable, the report by the Fédération des caisses Desjardins du Québec said.

Advertisement 2

Article content

Right now, Canada’s mortgage market is concentrated in fixed-rate mortgages of up to five years. Longer terms do exist, but they are a tiny fraction of the market.

Meanwhile, borrowers in the United States were able to lock in historically low rates during the pandemic for 30 years. Canadian borrowers who took out a mortgage at those rates have already had to renew at much higher rates or will have to do so in the next two years.

With Canadian households among the most indebted in the world, this extra burden comes at a particularly challenging time, Desjardins chief economist Jimmy Jean and macro strategist Tiago Figueiredo said in their report.

The difference in the two countries’ mortgage systems has been credited as part of the reason Canada’s economy has underperformed the U.S. in recent years. Canadians, more vulnerable to higher interest rates because of shorter mortgage terms, have cut spending or run up other debt to make ends meet, while Americans have continued to spend freely.

Jean and Figueiredo say the financial vulnerabilities could become acute if inflation flares up again and the Bank of Canada is forced to hike rates further.

Posthaste

Article content

Advertisement 3

Article content

“Suffice it to say that new interest rate hikes would deal a blow to households whose mortgage renewals are coming up, and there would likely start to be more forced sales and defaults,” they said. “It would be less the case if mortgages didn’t need renewals, or at least if they could be renewed less often.”

Other countries such as Australia and the United Kingdom also have shorter mortgage terms, but these markets have features that either ease the payment shock or avoid it altogether, Desjardins said.

For example, the U.K. has more flexibility in mortgage amortizations, allowing terms up to 40 years, which makes payments more affordable because they are spread out over a longer period of time. The downside is that a borrower pays more interest over the life of a mortgage.

In Canada, an insured mortgage typically can’t exceed 25 years, though 30-year amortizations are now permitted for first-time buyers of a newly built home.

Variable-rate mortgages dominate in Australia, making up about 75 per cent of the outstanding contracts, and most adjust immediately, unlike the fixed payments often found in Canada.

Advertisement 4

Article content

Australians experience their payment rises in real time, and as rate increases draw to an end, lenders there have not reported major increases in mortgage delinquencies, the report said.

But they have been rising in Canada. In Ontario and British Columbia, mortgage delinquencies are now above pre-pandemic levels.

“Our analysis shows that if the option to lock in 10‑year mortgage terms had been more prevalent and attractive, the payment shock would have been more manageable for households opting for it,” Desjardins said. “A 10‑year mortgage term would also make the stress test less necessary.”

Shorter-term mortgages became more attractive to Canadians in the 20 years after the great financial crisis because interest rates were in decline. However, borrowers in periods when rates were higher, including the past few years, would have also benefited from longer terms, the report said.

But in order to make longer terms more attractive to lenders and borrowers, obstacles have to be overcome.

Legislation on prepayments should be updated so Canada could then develop a “private-label” residential mortgage-backed securities market capable of supporting mortgage underwriting at longer amortizations as exists in the U.S., said the report.

Advertisement 5

Article content

The reason U.S. lenders are able to offer low rates on longer-term mortgages is their ability to package the debt and sell it to private investors.

“The bottom line here is that while there are frequent calls for stimulating innovation in Canada, the mortgage market is no exception,” Jean and Figueiredo said.

Before 2020, the Bank of Canada led efforts to innovate the mortgage market, but these were halted by the pandemic.

“The Canadian government is now in a position of having to urge lenders to show leniency towards borrowers facing mortgage renewal shocks,” Desjardins said. “This plea might have been unnecessary if better products had existed in the first place.”

“In our view, advancing this agenda has become more critical than ever.”

Sign up here to get Posthaste delivered straight to your inbox.

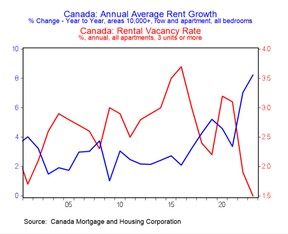

The plight of renters in Canada was flagged as a concern by the Bank of Canada in its financial stability report last week.

Senior deputy governor Carolyn Rogers said the share of renting households behind on credit card or auto loan payments is back at or above typical levels.

Advertisement 6

Article content

“And over the past year, the share of borrowers without a mortgage who carry a credit card balance of at least 80 per cent of their credit limit has continued to climb,” she said.

Extraordinary population growth led to falling vacancy rates that sent rents soaring, said Sal Guatieri, senior economist at BMO Capital Markets, who brings us today’s chart.

“Barring a cooldown, renters are at increased risk of getting priced out of many regions, much like prospective homeowners,” said Guatieri.

Advertisement 7

Article content

Moving your tax-free savings account from one institution to another seems easy, but there are rules to be followed. Tax expert Jamie Golombek has the details on one case where a taxpayer didn’t follow the rules and wound up with a penalty from the Canada Revenue Agency. Read more

Recommended from Editorial

Are you worried about having enough for retirement? Do you need to adjust your portfolio? Are you wondering how to make ends meet? Drop us a line at aholloway@postmedia.com with your contact info and the general gist of your problem and we’ll try to find some experts to help you out while writing a Family Finance story about it (we’ll keep your name out of it, of course). If you have a simpler question, the crack team at FP Answers led by Julie Cazzin or one of our columnists can give it a shot.

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Read them here

Today’s Posthaste was written by Pamela Heaven with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content