The Bank of Canada policy meeting may be a window into the U.S. economic cycle.

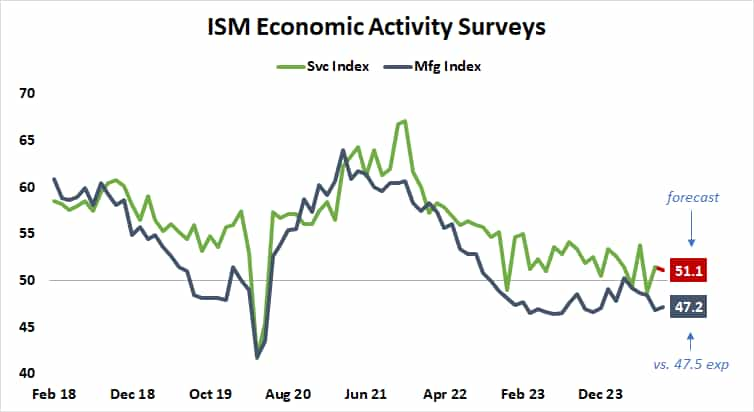

The ISM gauge of U.S. service-sector growth is seen showing steady expansion in August.

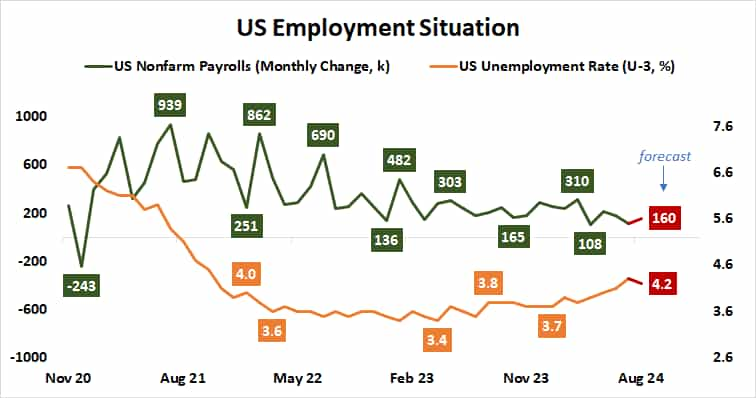

U.S. jobs data is expected to bring a hiring pickup after July’s disappointing slowdown.

Wall Street trading was muted in the final week of August. The bellwether S&P 500 stock index was little changed, rising a mere 0.2%. The tech-tilted Nasdaq 100 slid a touch lower, losing 0.9%. Such quiet—despite an earnings report from AI darling Nvidia (NVDA)—may speak to a lull in the markets’ top narrative: the outlook for Federal Reserve interest rate cuts.

Tellingly, bond markets were nearly motionless last week, with Treasury yields unchanged across maturities. Gold prices inched lower, and the U.S. dollar rose against its major currency counterparts. The yellow metal rose and the greenback fell as yields slumped in the previous week.

A slew of key Fed-relevant data points is on the docket for this week, promising to offer markets fresh fodder for speculation. With that in mind, here are the macro waypoints likely to shape what comes next.

The Bank of Canada is widely expected to issue a third consecutive cut of its target overnight interest rate this week, lowering it by 25 basis points (bps) to 4.25%. This is after inflation slowed to 2.5% year-on-year in July, the lowest in over three years, and despite a pickup in economic growth in the first half of the year.

The markets are pricing in a target rate of 3.76% by year-end, implying 74bps in further easing. That amounts to three more standard-sized 25bps cuts. Canada’s economy is intimately tied to that of its southern neighbor, so further dovish guidance may stoke U.S. slowdown fears. Close to 80% of Canadian exports are bound for U.S. markets.

Analysts expect to see that the pace of service sector activity growth held broadly steady in August when the Institute of Supply Management (ISM) publishes its latest survey this week. A shock contraction in June was followed by a rebound in July, and last month’s performance is seen broadly keeping pace.

Services make up the biggest contribution to U.S. economic growth, accounting for over 70% of demand. This makes performance here a critical input for market-watchers and central bank officials alike. An outcome broadly in line with expectations may cool bets on a 50bps rate Fed rate cut next month, weighing on stock markets.

The August U.S. jobs data has taken on particular significance after the Fed loudly signaled September is the start of the rate-cut cycle. Fed Chair Jerome Powell and company spent most of July and August laying the groundwork for a policy pivot, arguing the risk of too-high unemployment has grown to be nearly on par with that of too-high inflation.

The figures are expected to show the economy added 160,000 jobs last month, marking a pickup from the soggy 114,000 in July. That dour reading triggered rapid selling across global stock markets. The unemployment rate is penciled in at 4.2%, a slight downtick from 4.3% previously.

As with the ISM data, traders are likely to focus on what the numbers mean for the likelihood of a double-sized 50bps rate cut at next month’s fateful meeting of the policy-steering Federal Open Market Committee (FOMC). The priced-in probability of that outcome now stands at 37%. Wall Street may jeer if middling data makes it seem less likely.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

in 2024 – a year in review")