The Canadian market has experienced significant volatility recently, with stocks recovering impressively from an early August correction, supported by a resilient economy and positive earnings growth. As tech heavyweights face headwinds from lofty expectations, investors are increasingly turning their attention to high-growth opportunities in the broader tech sector.

|

Name |

Revenue Growth |

Earnings Growth |

Growth Rating |

|---|---|---|---|

|

Docebo |

14.74% |

34.09% |

★★★★★☆ |

|

Constellation Software |

16.17% |

23.55% |

★★★★★☆ |

|

HIVE Digital Technologies |

54.20% |

100.27% |

★★★★★☆ |

|

Wishpond Technologies |

12.72% |

113.87% |

★★★★☆☆ |

|

GameSquare Holdings |

38.08% |

86.64% |

★★★★★☆ |

|

Medicenna Therapeutics |

62.37% |

57.20% |

★★★★★☆ |

|

Cineplex |

8.05% |

179.27% |

★★★★☆☆ |

|

BlackBerry |

20.61% |

76.74% |

★★★★★☆ |

|

Sabio Holdings |

12.97% |

122.50% |

★★★★☆☆ |

|

Alpha Cognition |

62.98% |

69.54% |

★★★★★☆ |

Click here to see the full list of 22 stocks from our TSX High Growth Tech and AI Stocks screener.

Let’s review some notable picks from our screened stocks.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Cineplex Inc., along with its subsidiaries, operates as an entertainment and media company in Canada and internationally, with a market cap of CA$697.34 million.

Operations: Cineplex generates revenue through three primary segments: Media (CA$120.16 million), Location-Based Entertainment (CA$132.08 million), and Film Entertainment and Content (CA$1.05 billion). The company operates in Canada and internationally, focusing on various entertainment services.

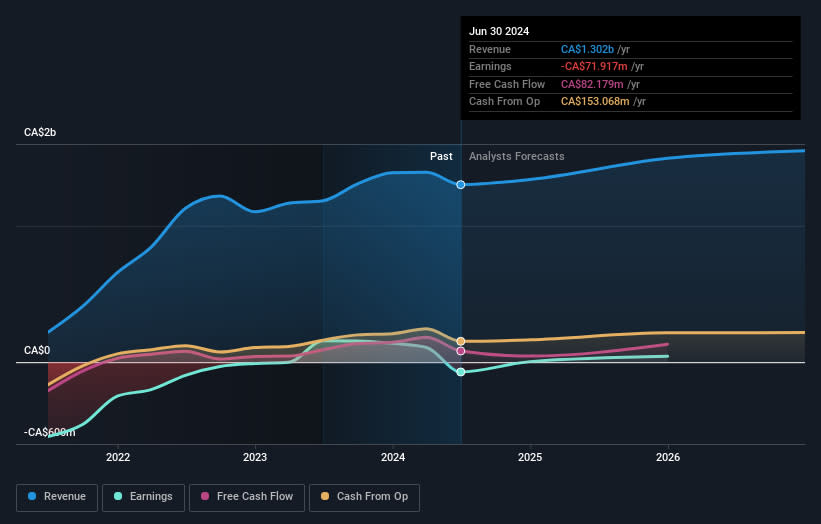

Cineplex’s recent earnings report shows a significant net loss of CAD 21.44 million for Q2 2024, contrasting sharply with the CAD 176.55 million net income from the same period last year. Despite this, revenue is forecasted to grow at an annual rate of 8.1%, outpacing the Canadian market’s average growth rate of 6.9%. The company’s share repurchase program aims to buy back up to 6,318,346 shares by August 2025, potentially bolstering shareholder value amidst fluctuating financials.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Computer Modelling Group Ltd. is a software and consulting technology company that develops and licenses reservoir simulation and seismic interpretation software, with a market cap of CA$1.04 billion.

Operations: Computer Modelling Group Ltd. generates revenue primarily through the development and licensing of reservoir simulation and seismic interpretation software, amounting to CA$90.29 million. The company also provides related consulting services, contributing to its overall financial performance.

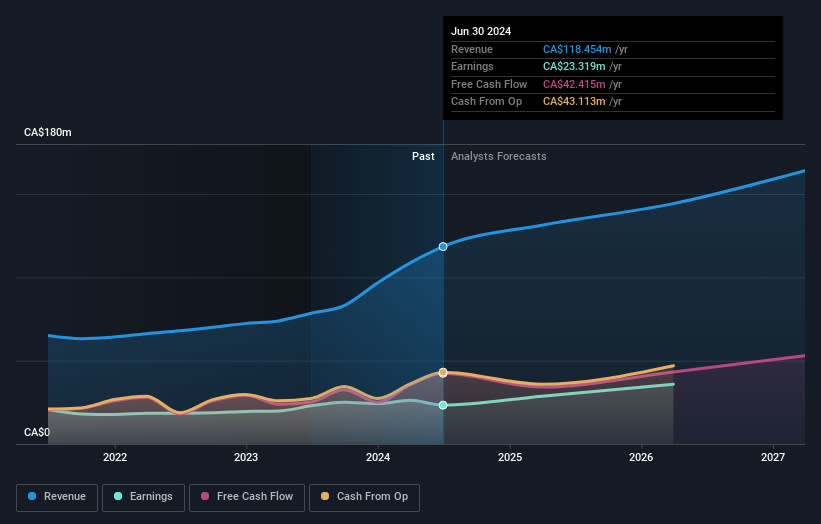

Computer Modelling Group (CMG) has demonstrated robust revenue growth, with a forecasted annual increase of 11.5%, outpacing the Canadian market’s average of 6.9%. The company’s earnings are expected to surge by 24.6% annually, reflecting its strong R&D initiatives and innovative solutions like CO2LINK for carbon capture and storage (CCS). Despite a net income drop to CAD 3.96 million in Q1 2024 from CAD 6.9 million the previous year, CMG’s strategic projects such as the Trudvang CCS project highlight its potential for long-term value creation in sustainable technologies.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Stingray Group Inc. operates as a global music, media, and technology company with a market cap of CA$537.31 million.

Operations: Stingray Group Inc. generates revenue primarily from its Radio segment, which contributes CA$154.41 million, and its Broadcasting and Commercial Music segment, which brings in CA$201.10 million.

Stingray Group’s recent Q1 2024 results revealed a sales increase to CAD 89.07 million from CAD 78.99 million, though net income dropped to CAD 7.3 million from CAD 14.12 million the previous year. The company repurchased 737,200 shares for CAD 4.57 million since September 2023, reflecting strategic capital allocation amidst its evolving business model. Notably, Stingray’s R&D expenses have been significant in driving innovation; the firm’s revenue is forecasted to grow at a rate of 4.9% annually despite industry challenges.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include TSX:CGX TSX:CMG and TSX:RAY.A.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com